Enphase | Q3-24 Earning & Call

The light is getting brighter.

The tunnel was very long, but we might finally be reaching the end - although the market hardly disagrees as the stock fell 15% since last night.

Overview.

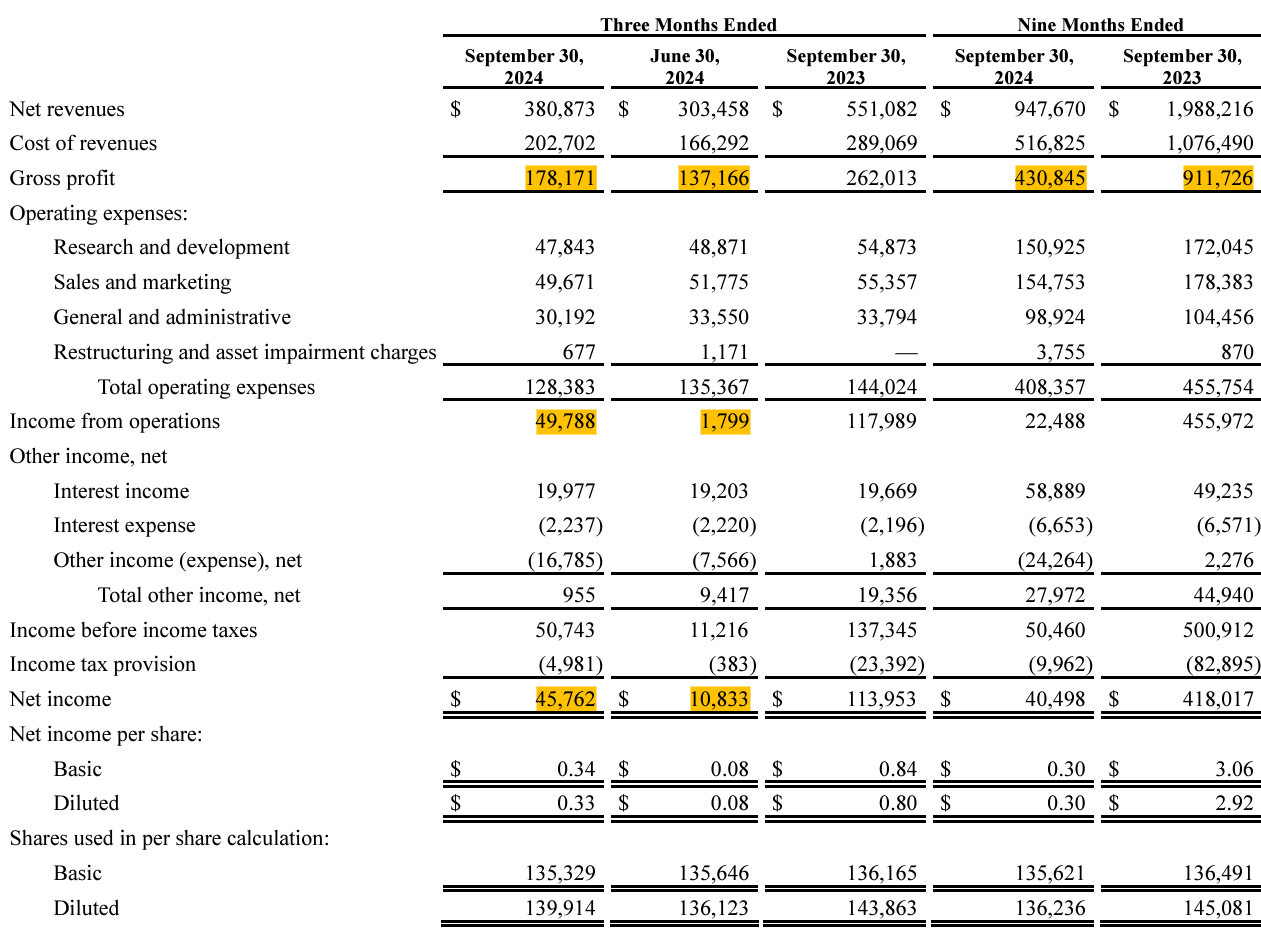

EPS. $0.77 | $0.65 | -15.58% miss

Revenue. $391.98M | $380.87M | -2.83 miss

$49.8M of buybacks.

“Looking ahead, we see lower interest rates, ITC adders, and higher power prices as the key drivers for 2025 growth.”

Everything is still red, but the YoY comparison isn’t interesting to make as lots have changed economy-wise since Q3-23.

Business.

The company delivered 1.7M microinverters and 172.9 MWh of batteries, a strong decline YoY for the first one and big growth for the second. This is explained by a higher attachement rate for batteries in the U.S., especially California.

The comparison is much better QoQ or with early 2024 when difficulties started for Enphase and our economies at large - when interest rates were already high. Many see a declining company but I see a quaterly improvement and maybe the start of better times although predictions are dangerous… Unpredictable things happened and will continue to happen.

“So, basically, a few months back, we didn't anticipate the installer bankruptcies, one in the U.S., we didn't anticipate the European business declining further.”

The FY-24 narrative was that installers had lots of inventory and didn’t need to buy more as demand slowed and they had to destock. This narrative is over in the U.S., but still accurate in Europe for different reasons depending on the country.

Enphase reaffirmed its capacity to manufacture more than 5M microinverters per quarter in the U.S. alone, infrastructure they wouldn’t maintain if they thought the potential volume was too high long-term. They already closed factories and would do so again if they didn’t need them long term.

They also talked about their EV chargers which are, as electrification is growing, becoming a significant part of the demand. They estimate their SAM to be about $1.4B in the 14 countries where they intend to introduce them.

Rapid overview of the quarter business-wise; the U.S. is back to a healthy state with a lower but growing demand QoQ. Europe is still struggling due mostly to a terrible macro environment & some regulatory concerns. Expansion is going well, but these countries will take time before becoming significant. The company is still hard working to improve its product and deploy them in different geographies or to improve its relations with installers.

Numbers aren’t great by themselves. But the narrative is now better.

Geographies & Use Case.

This part can be seen as a small bull case for Enphase products globally, although the need is different depending on the geographies.

They are present in 51 countries and more will come before EoY but most of them are new and Enphase isn’t fully established there yet - India, Australia and some southern European countries... strong potential geographies where Enphase is slowly growing its influence.

India.

Each geography has a different need for solar energy. In India, for example, it is a matter of comfort as infrastructures aren’t developed enough.

“… and in India, if you didn't know, you lose power five times a day [...] And so, it's a beautiful solution for many of the luxury builders, where they can build it into the -- some of the homes which can cost anywhere from $200,000 to a couple of million dollars. They can build it into the home and raise the value of the home and provide complete energy independence.”

We could make the case that this might be a short-term problem as infrastructures will be built and India now has access to cheap energy from Russia, paid in its own currency which will change everything for the country. But by the time infrastructure is built, many might already be using solar energy for the independance it offers or to help power the grid during its beggining.

huge market, huge potential and faster to install a solar system than to wait for infrastructures.

Europe & France.

The same Russian energy that is sold to India isn’t sold to Europe anymore… And solar energy in Europe is slowly becoming a necessity for households - in my personal opinion and only for some countries.

I’ll take France as an example where electricity prices rocketed following the war in Ukraine and the government took measures to limit what households would pay; electricity prices above a limit would be covered by the state - future taxes, that is. This measure is coming to an end in 2025 and if electricity tariffs were lowered in 2024, we’re looking at double-digit increases - up to 50%, in 2025. With Russian pipelines and geopolitical conditions as they are - both in smoke, there is no hope to see these prices decline in the medium term.

Not even entering into discussions about overall energy agreements in Europe where France has to provide other countries with cheap electricity because others closed their nuclear power plants and cannot generate enough for themselves.

So, based on this month’s data.

“With the average household in France consuming about 4770 kWh electricity (in French) in 2024, the average annual electricity cost in France ranged from 1057€ - 1723€, depending on the electricity provider and plan chosen.”

If prices were to grow only 25%, you’d be between €1,321 and €2,153 while the installation of solar panels in France is between €2,000 & €2,500 per kWc with 4kWc enough to power a 100m house - so a €10,000 installation give or take, without batteries. Those are very rough calculations and you’d probably not have full autonomie there but it gives an idea, without taxes advantages here.

You can do the math; over a ten-year timeframe, there are no questions about which solution is best financially - not even considering the peace of mind of autonomy.

Everything to say that even if Europe is slowing down lately, I do not see a world where solar energy & autonomy don’t become normal in most countries there. Those who can borrow money when interest rates finally lower will certainly do so to install these kinds of systems, or suffer crazy bills .

Revenues.

As shared earlier, the YoY comparison is painful in terms of business & financials too - we’re talking about a -53% decline in revenues YoY for the nine months ending.

But we are also with strong growth QoQ sourced from growing demand of their products with revenues, operating revenues & net revenues growing respectively +29.9%, +2,667%, & +322%.

The numbers are a bit ridiculous but they clearly show short-term improvement. Margins are very reasonable and also show short-term improvement while the balance sheet remains strong with $470M of net debt; the storm is almost past, the company stayed profitable & cash flow positive.

We can also talk about buybacks as Enphase still has $598M on its current plan which corresponds to more than 5% of the company at today’s valuation.

A healthy company altogether.

Guidance.

The outlook is still pretty weak as management remains unclear about how Europe will turn out short-term.

“We are cautious for Q4, this is why our guidance incorporates a slowdown in Europe in Q4, and we are not pushing more into the channel.”

We’re talking revenues between $360M & $400M Q4-24 for FY-24 revenues around $1.3B, down -43% YoY.

My Take.

It’s time to do some math and take some risks; look inside the crystal ball. You understand that I am bullish on electrification globally & on solar panels for different reasons - be it necessity like in Europe or comfort like in India.

Enphase has a better technology; there’s proof of concept & demand. It is expanding geographically to countries where there is a need for their products & macro conditions in the West are improving as both the U.S. & Europe are cutting rates. All these factors should make 2025 a better year.

Making some assumptions from here: FY-24 should come, as said above, with $1.3B revenues. Guidance under current macro conditions suggests $360M as a low end for Q4-24 so I would assume - with everything we discussed, that this should be the lowest point short term; thus FY-25 should come with at least $1.44B - a 10% growth YoY.

Things should improve from there so above 10% CAGR up to 2026 should be pretty conservative.

At today’s price we’d be slightly above historical P/S ratios although it doesn’t seem unreasonable to have an ~8x P/S ratio; I still could understand why one might want a better entry point - especially in such a competitive industry. Reaching a 7x P/S based on above assumptions would mean an entry between $60-$65 which represents an important region in terms of price action.

A potential 20% / 25% decrease from today’s price seems entirely possible short term but I personally wouldn’t count on it. We’ve potentially seen the worst and I’m not sure we have many sellers left after today but I could be completely wrong here. But if management is right and bottom is passed, there would be no fundamental reasons to sell more.

I believe it’s all about investment timeframe & narrative from now. The quarter isn’t good but it shows strength & signs of a potential rebound. I personally believe in electrification & households' need for independence. Enphase has technology that distinguishes itself from competitors within an highly competitive industry; if one wants to invest over five years or more starting here - and averaging down if prices decline, it seems like a good idea. It also makes sense to me to wait until we have concrete data showing improvement for the company’s products’ demand - even if it means buying at slightly higher prices.

There are no definite answers in the stock market. Only a different risk/reward balance for each of us, but I personally believe we're in a good spot to slowly start accumulation here with a 5-year timeframe or so.