Duolingo Q2-25 | Earning & Call

Thank you Mr Market.

If you guys are interested, you’ll have 15% discount on FiscalAI subscriptions through my referral link. FiscalAI is the tool used for KPIs on all my write-ups, really powerful, valuable data & great UX.

https://fiscal.ai/?via=wealthyreadings

Everything you need to understand Duolingo's bull thesis is here.

As shared many times, Duolingo is aiming to become a global learning platform.

All of this brings us one step closer to our mission, to develop the best education in the world and make it universally available […] And now we're also adding other subjects. I mean there's hundreds of millions of people that are interested or already playing Chess. The same is true for Math, the same is true for Music. So I just don't think that we're anywhere near our full TAM.

Business.

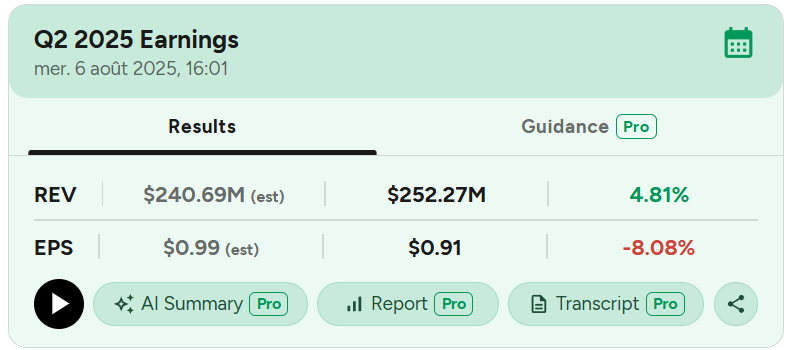

A strong quarter for Duolingo, although we could call it a logical continuation. Some of its strength also comes from timings, which is important to keep in mind as it means next quarters might look a bit weaker - only look.

User Base.

The market sold Duolingo the last months due to a boycott which raised concerns on onboarding & retention, coupled with the global concerns that learning a language is useless or that AI is going to make speaking irrelevant. I'll let you read my investment thesis for those subjects. The bottom line remains that Duolingo is an online global learning app whose first business is language learning.

And it's already a huge one.

There are 2 billion people learning a language in the world. We have about 130 million active users, give or take. And so there's a lot of room there

And data proves that demand is not slowing with stron onboarding, retention & conversion.

There are some comments to make on both MAUs sequential decline & the strong DAUs sequential & YoY growth which are due partly to the boycott I talked about earlier and partly to the Dead Duo campaign.

On the positive first, the campaign was a massive success - as shared last quarter & attracted tons of new users until the end of February, hence the strong MAUs growth during the period which logically ended in a slowdown this quarter – you can't always have massive acquisition. What matters is that lots of those new users ended up using the app daily for a few more months, shown with the DAUs growth.

Duolingo attracted a massive amount of new users due to its campaign and some left after a few days or weeks. But most stayed and became DAUs. And many even turned to subscribers.

Duolingo's retention & conversion ratio is a thing of beauty, and onboarding is really healthy but dependant on marketing campaigns' timings, which is normal.

This explains most of the user dynamic between both quarters and it could impact Q3 as there are lots of really fresh users who might not stay despite Duo's pressure. Plus the summer holidays,, beach, bikinis, daiquiris & summer loves...

There are forces against which even an angry owl is powerless.

To remain serious, summer is not a weak season historically for Duolingo so it should not be an excuse for a weak Q3. This marketing timing partly explains the slow down in MAUs growth this quarter, with the second part being the following.

On the negative, there was some backlash & a Duolingo boycott after Luis, the CEO, shared an internal communication where he explained his desire to make Duolingo an "AI-first" company, which many (stupidly) interpreted as "we'll fire everyone". I won’t comment with my personal opinion & will only share management's comments.

I should say, the effect of that was essentially all in the United States. And when I say United States, that includes Canada and stuff like that. But it's essentially all in the United States, and among young audiences

This "mistake" slightly impacted Duolingo's users as some thought that canceling their subscriptions would help change the world. Damages were limited and management learned its lesson: do not share internal communications publicly as the public doesn't necessarily understand what internals do.

So we stopped posting edgy posts on our social media and we started posting things that we thought would get our sentiment more positive. And that has actually worked. By now, the sentiment on our social media channels is all very positive. But we still are not posting the extremely edgy things that are more likely to go viral.

Edgy & viral are Duolingo's ADN and management confirmed it will come back but they'll wait some time.

To clarify – if necessary, what Luis meant was to leverage AI to boost efficiency and deliver more/better content. Nothing else.

Content.

First, management confirmed they had no plans on bringing new subjects onto the platform – not immediately that is. They will focus on upgrading what exists before adding new verticals.

We also had some feedback on Chess & content in general.

It's just grown a lot. And it's a project that has gone really fast. I mean 1 year ago, exactly 1 year ago, we had not even written a single line of code for Chess in our app, like this project had not started. And within a year, less than a year, we launched it and it's there on iPhones now and it's been growing. And when you restrict only to iPhones and only to English user interface, already Chess has surpassed Math and Music. So we're seeing a lot of demand for that and we're very happy with that.

This is only an example, but a great one for how fast Duolingo can create, deploy and soon enough monetize a new subject as in time, the subscription models will change, as I shared in my investment thesis.

The thing that we do is we just we want to be cautious about particularly investors getting very excited about the amount of revenue that these courses are going to provide. Because at the moment, we're just selling everything under the same subscription and we're not even trying to optimize revenue for Math, Music or even Chess. So we're very excited. We think this is really going to help us grow the TAM because it's going to get way more people to want to use our product.

My base case would be some bundles for X subjects or per subject like Adobe does with its softwares; but we are still far from this.

Subscription plans.

Management has made lots of tests over the last quarters on free and paid users, to measure engagement, conversion & more. They recently changed the mechanism of their freemium with positive feedback in term of data.

The original system had hearts, allowing users to do any lesson they wished until their hearts ran out with each mistake, giving them options to wait, pay or watch a publicity to recharge them. The new system has 25 points of energy which will be consumed per exercise while correct streaks will generate free energy – until they run out and can refill exactly like before.

So what's really nice about it is that, for the average user at least, we've substituted a carrot for a stick. So it used to be the case that every time you made a mistake, you lost something. Now if you don't make mistakes, you gain something. So that's actually quite rewarding. And what we have seen when we're rolling this out is that this increases revenue, our bookings, and both. It increases daily active users. And it increases the median time spent using the app. So we're really happy with this. We've been rolling it out.

The freemium is the first step to retention and later converstion, so playing on users' phychology with different methods will yield different results. And this new method is better for Duolingo’s metrics, despite some complaints, as expected.

Whenever we do a major switch to a mechanic on Duolingo, there's a number of people that don't like the change. One of the things that happens is that Duolingo is a habit-building app. We build a habit to use Duolingo every single day. And the thing about habits is you want them to be the same every single day. That's what people like.

Management knows its stuff, and its business.

Some words on Max, which has been growing well, slightly under expectations, but management has great plans for the AI subscription and I personally remain really bullish about it.

The percentage of subscribers that are Max subscribers - a couple of quarters ago, it was 5%, then last quarter it was 7%, and then in Q2 it was 8%. So it's been growing. It actually grew a little less than we expected. But part of the reason for that is because Super grew even more. So it's just a fraction between those 2. Super just is kind of performing even better than we expected.

One of the fundamental reason of the slower growth is just that Max isn’t adapted to everyone yet. It is a conversational tool which means it requires a certain level already. But management is working on upgrading it.

So one of the things we're going to be experimenting with is having a conversation that is bilingual. So if you're an English speaker learning Spanish, some of it is going to be in English, some of it is going to be in Spanish, to kind of ease you in. We're also going to be working on making the conversations more engaging.

This is the beginning for Max. Conversion & retention matters, but what really matters is the improvement of the feature itself, in terms of usability & performance.

Now we have a really good metric that we're optimizing for, which is average number of words spoken per Max subscriber. And it's a really good metric because we can move it and because it exactly captures what we want people to do, which is to speak more. And ever since we started optimizing that, I think our Video Calls just started getting better and better in the sense that now the models are starting to learn that it is better to do things to keep you engaged. So asking more questions, et cetera, to keep you engaged, and also asking you open-ended questions as opposed to yes/no questions to get you to practice more. So that's the type of stuff that we're doing, and I'm very happy with the progress.

Improvements are coming, and they look really great.

China & Geographies.

China is growing above expectations, partly thanks to another marketing campaign with the biggest coffee franchise in the country.

We feel really good about China. It's our fastest-growing market. We've been growing a lot. We had a really incredible partnership, this time around with Luckin Coffee, where, for a couple of weeks -- Luckin is like their Starbucks. It's everywhere. For a couple of weeks, a lot of their stores were basically decorated with Duolingo and had Duolingo cups, and there were drinks named after Duolingo and everything. And that was a pretty big boom

More Chinese users and still no Duolingo Max in China as any LLMs used there has to be built on Chinese technologies – which will probably be Alibaba's as it has the best models. Management is working on adapting its models so it will be available in some time - no dates were given.

On other geographies, management is planning to spend on marketing in the U.S. - the slowest-growing revenue source, after some positive experiments in Mexico.

Growth was comparable in the region as management only relied on its social media platforms, and they decided to spend a little bit to see the impact - some influencers and more classic advertising. Results were rapid & strong, and it encouraged the team to try the same in the U.S. to boost growth - although the need to learn english, their biggest market, is obviously lower there...

Apple & App Stores.

We talked last quarter about the potential ruling that payments executed through web pages on smartphones would be exempted from the store fees – of 30% for Apple, a game change for many apps owner, Duolingo included.

But so far, the testing shows that we can send people to a web purchase flow, minimally lose bookings - we do lose some bookings by sending people to an external purchase flow because there's more friction. But it really significantly increases our profit.

We have not done the full push to all our users on that. But you'll likely see us do that.

The ruling is not definitive yet but once/if confirmed, it would make a big difference for 2026, 2027 as Duolingo's subscriptions are mostly yearly, meaning renewals will only happen later on.

We will have answers at the end of the year for the ruling, but this would be massive financially for app owners, with stronger revenues & margins.

Financials.

And we won't find anything wrong here either.

Revenue growth is impressively stable around 40% since four long years, the same can be said for gross margins and net margins are now improving thanks to many factors, mostly due to higher revenue base & improved efficiency, leading to the highest net income of the company's history. And we could expect net margins to expand much more as AI usage grows with lower cost per token due to the rapid improvements in the industry, plus the potential modifications with the App Stores.

I'll also note that Duolingo is used all around the world hence paid in many different currencies, and with the dollar falling during Q2, the currency mix has also helped for both growth & margins. This is outside of the company's control, but it's important to be aware of it as it will fluctuate.

In terms of cash, Duolingo generated $86M of FCF including $65.6M of SBCs and has a net debt of $1B, really comfortable in terms of cash & cash generation. Some could complain about the dilution as total shares are up 4.5% YoY, but I guess it is a subject which will be addressed soon, now that profitability is stable.

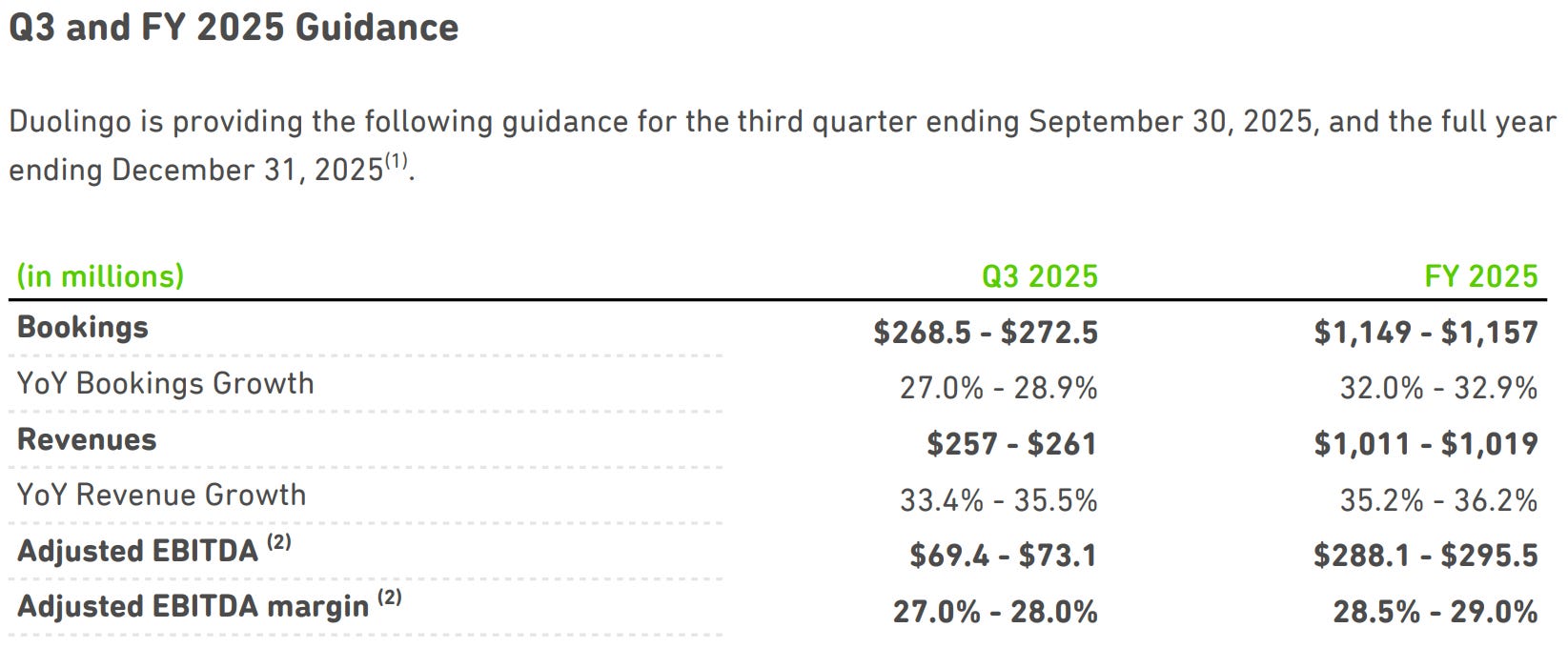

Guidance.

Management raised guidance after this quarter.

Continuous growth & growing margins.

As a result, we're raising our full year guidance again, while still investing in both our core business and exciting new areas like Chess, Math and Music that we believe will drive long-term growth.

Investment Execution.

This quarter looks really impressive because of the stock reaction, but the truth is it is not. It is a great quarter of continuation after years of great quarters. It continues to confirm my personal investment thesis & I am glad the market overreacted these last weeks and gave me the opportunity to build a pretty big position on the name - my second biggest one after this 25% plus reaction. Every data point points towards the good direction. So let's just say thank you to Mr. Market.

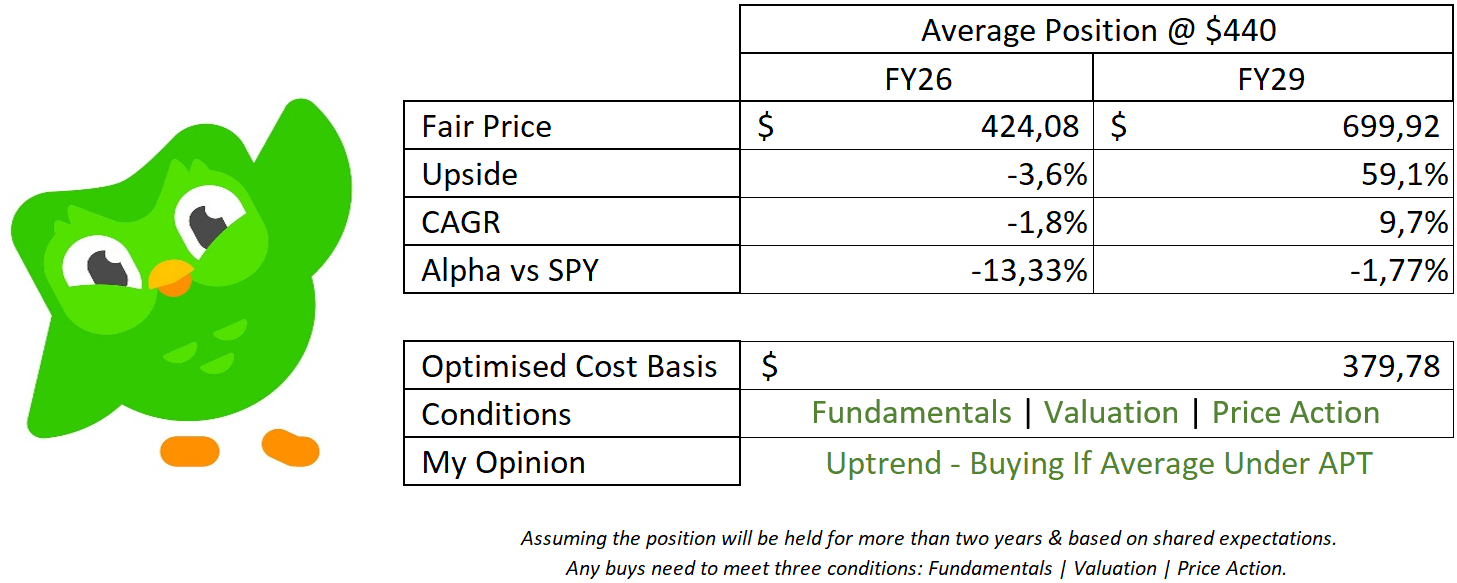

This model assumes a 32% and 25% CAGR growth until FY26 and FY29, respectively, 19% net margins, no dilution, and a P/S at 16x, slightly lower than Duolingo average.

I did not change my valuation model which is slightly more conservative as guidance was raised, making short term targets easier to reach - 28% revenue growth FY26 to reach it. It isn’t a given though and will require execution but with the short term levers the company has, it seems more than doable.

In terms of price action, the stock created a massive gap at earnings so I wouldn't be surprised to have some chopping, some red days to compensate.

This might not happen at all though, last quarter went straight up for days. What I mean is to not be surprised if we give back some of those gains.

A very happy shareholder who will gladly accumulate on opportunities.