Celsius | Q3-24 Earning & Call

There's more behind the smoke.

If you do not know about Celsius, everything you need is here.

Overview.

Quarter is as tough as we could have expected.

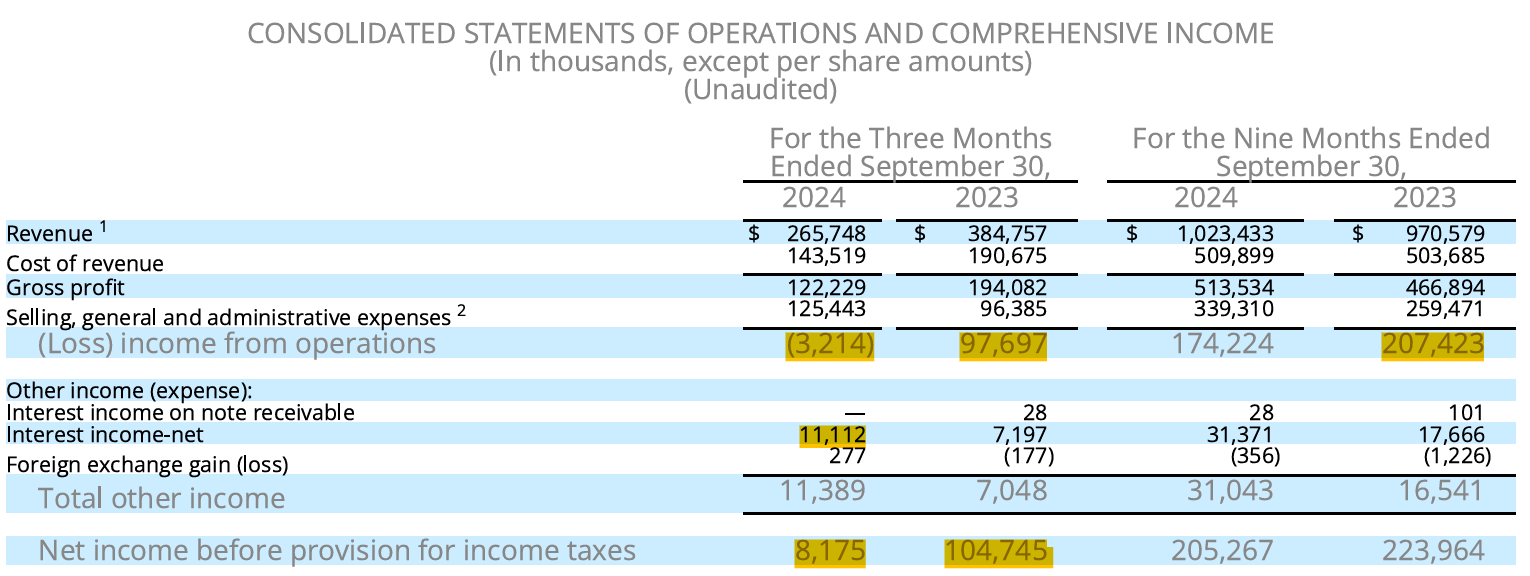

EPS. $0.03 | $0 | miss

Revenue. $267.11M | $265.75M | -0.51%

“Pronounced supply chain optimization by our largest distributor, which we believe has largely stabilized, had an outsized and adverse impact on our operating results during an otherwise solid quarter.”

I am not sure about the “otherwise solid quarter” but this tough quarter could have been - and was, expected.

Business.

The energy drink industry is struggling lately and this isn't just a Celsius thing. This is a global tendency affecting all brands which Celsius attributes in part to reduced foot traffic, otherwise to tougher maccro & consumers.

“We saw a lot of our major retailers talk about reduced traffic and convenience.”

It’s an important introduction because part of this quarter’s weakness comes from there and affects everyone, and demand for those products has a cyclicality we cannot ignore.

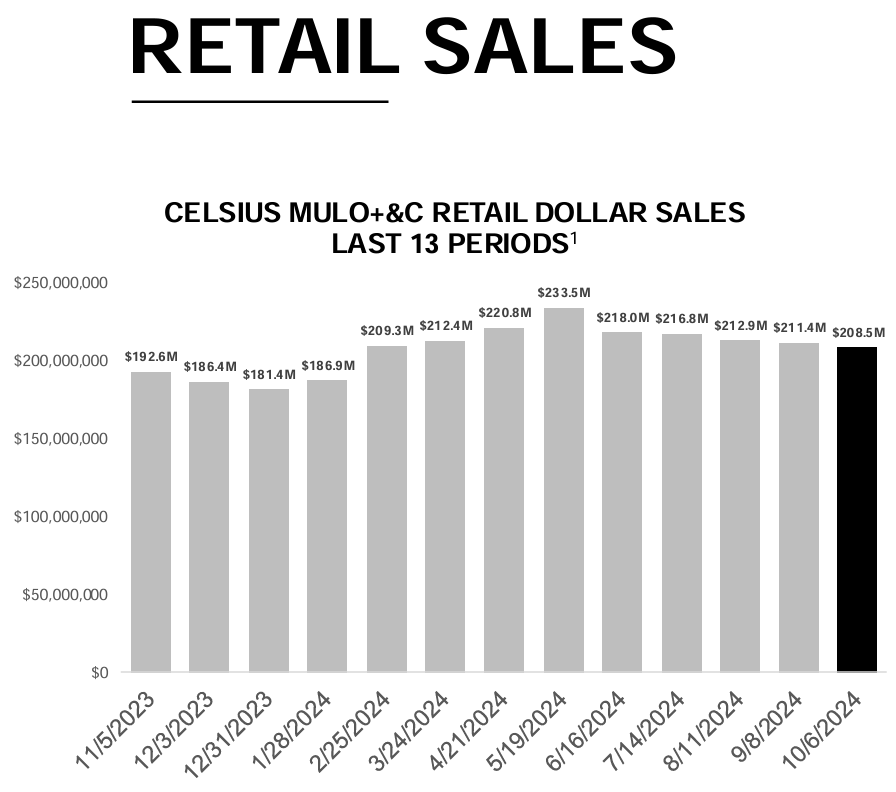

About Celsius, I am interested by only one metric at the moment: the retail sales and to be honest, the data isn't bad - and only includes the U.S sales.

Why only this metric? Because Celsius acknowledges revenues when its products are bought by resellers, not consumers. With the actual inventory issues, Celsius' revenues are no indicators for demand or growth, only the retail sales are - as they indicates the volume of products sold to final consumers.

As you can see, we are above FY-23 total retail sale with one quarter left so we’ll very probably see growth during the year. Hard to say how much but it wouldn’t be surprising to see a continuation around $200M or so per month while October already closed above $200M.

This would bring FY-24 around $2.8B, up 27% YoY and around $350M of revenues for Celsius from U.S resellers for the next quarter - and assuming no inventory issues, to which we need to add international & other resellers revenues.

But we all can see those six months of consecutive declining sales which could be attributed to seasonality or as Celsius said, to a lower global demand which could rebound early next year… Very hard to know, although Celsius is still doing better than the industry's average.

“Celsius retail sales in the quarter ended September 30th increased 7.1% year over year on unit sales increase of 7.3%. Celsius resilient growth at retail overcame softness in the category, which grew at 2% in the same period.“

We also have a small decline in global market share for the first time since many quarters now, the question is the same: small bump or bigger issue?

Pepsi's inventory is supposed to be emptied or close to be by now and we should have revenues equaling sell through in Q4, with a $15M, give or take, potential impact.

“So we've got a handful of weeks of visibility into the Q4. We're definitely seeing a tighter correlation on a weekly basis between the inventory sell in and depletions from our largest distributors' warehouses into retail when comparing to Q3. It's not fully matched yet. So there is a slight disconnect from the sell through versus a sell in with retailers, but it's very slight at this point in time.“

The company purchased its long-time co-packer Big Beverages Contract Manufacturing for $75M for different purposes.

“The strategic transaction provides Celsius with a 170,000-square-foot, modern manufacturing and warehouse facility that is expected to provide greater supply chain control, quicker innovation cycles and greater production exibility.”

They only acquire infrastructures they used at 100% of its capacity to reduce costs over the long term.

Revenues.

Those are bad. But do they matter?

The YoY growth was to be expected as management already talked about the $120M-ish hole in revenues due to Pepsi's inventories.

The gross margin decline is primarily due to Pepsi’s inventory optimization as much as from some incentives, and Celsius plans to continue doing some until at least end of year, putting more pressure on them. It’s the cost to acquire more clients and force consumption in a time when consumers are turning away from those products.

The net income decrease is the most concerning issue but explained by lower revenue growth. They chose not to cut any expenses and proceed normally, as if Pepsi was still stocking. The optimist would say that without these inventoriy issues, net income would be up around 40% and it’s not wrong. The pessimist would say it wouldn’t be a profitable quarter without interests and they’re also right. I personally believe it does look ugly but it really is a false problem.

Balance sheet remains strong with $900M of net debt and positive OpCF & FCF.

My Take.

This is a very complicated quarter to comment & conclude. Part of me feels like I am holding to hope more than to data while another part remains optimistic on the business as most of what is happening isn't due to any issue with the products for now. There is a slowdown but nothing worrying.

The bull side is that the retail sales are still growing YoY very correctly, up more than 30% for the entire business. Celsius' market shares in the industry are stable but the sector itself is getting roughed by a lower demand - which always comes back. International expansion is ramping up rapidly and bringing good revenues & growth, which should accelerate. Lastly, the inventory issue which is the principal cause of the bad situation is coming to an end this year, leaving Pepsi with a fully optimized supply chain - with sell in comparable to sell through.

On the bear side, we probably won't have more than a single digit YoY revenue growth and even if this is a short term bump because next year's inventory issue will be dealt with, we'll still have the consumer problem, the low demand for energy drinks, entering winter & potential drop in market shares…

I personally chose to look at the retail sales data because this is what translates the real demand for Celsius' products at the moment, as revenues are impacted by inventory. Once this is gone, we could talk about minimum 15% increase in revenue without any sales retail growth, only because of optimized inventories.

We could easily have a double digit growth in FY-25 without any increase in demand, simply due to inventory optimization & easier comps. This would bring something between the base & bull case FY-26 with a slightly better environment - which should happen. Those are pretty conservative assumptions and would need a low P/S ratio to give us our required return.

The strong balance sheet of the company & its profitability are two reasons why I am holding but this investment might stay dead money for a few more quarters and relies on the company keeping its market shares stable over the next quarters. This is what most investors will look at.

I might be wrong, might refuse to see the truth, and I'd understand if someone wanted to sell their shares for a better asset. But as long as the retail sales are positive, I blame the bad financials on the inventory issue. As for buying… A small DCA might not hurt if my thesis is convincing but I'd rather stay out or put my cash on another asset if I were not already in…

But I’ll personally be holding a bit longer.