Airbnb | Q4-24 Review & Call

Business as usual.

If you do not know about Airbnb or its bull case, you will find everything you need right here - a pretty cool read.

Overview.

I didn’t board on the excitement train the market started for this quarter. It is a good quarter, data is correct and the company continues on a positive trajectory. But nothing more.

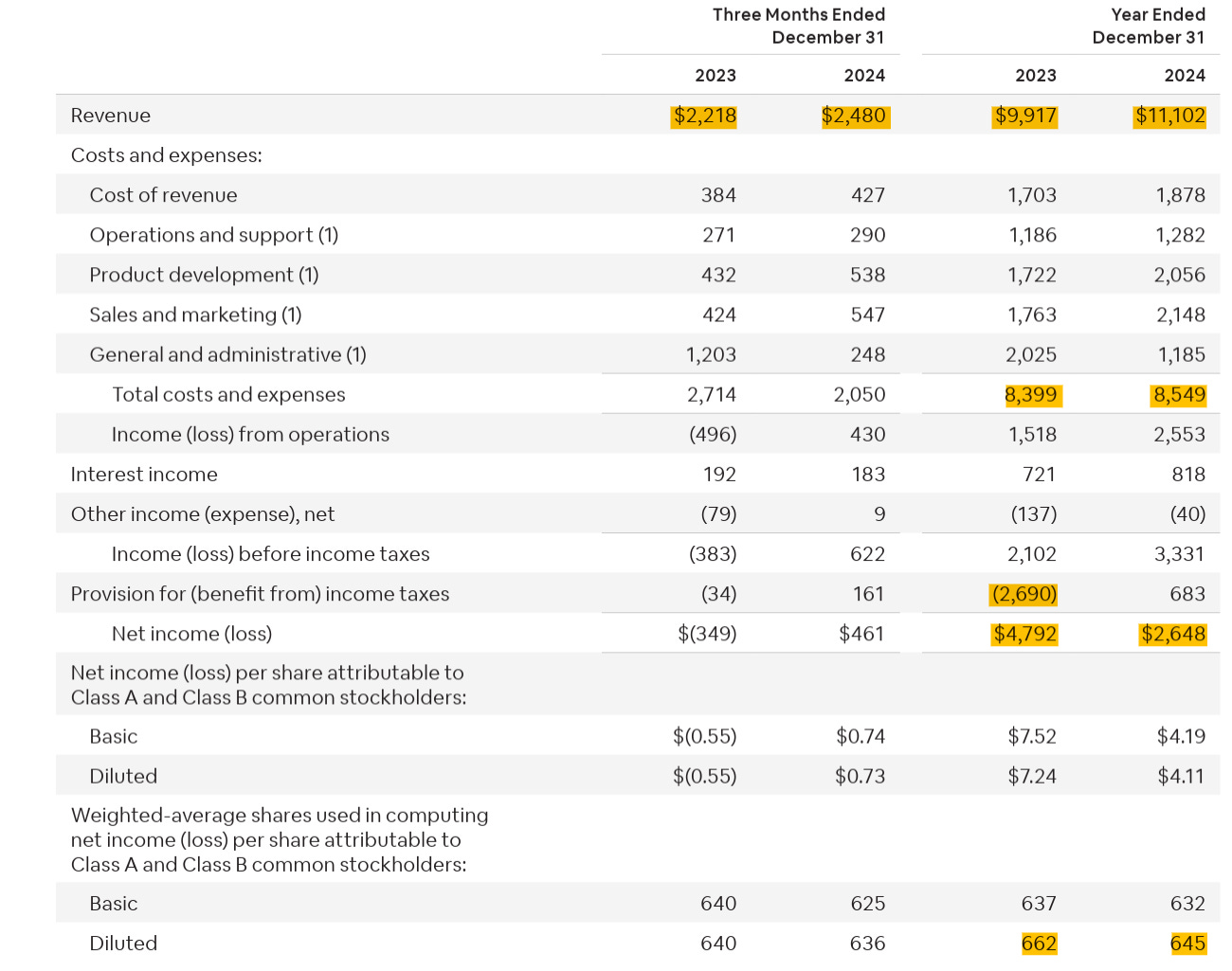

Revenue. $2.42B | $2.48B | +2.48% beat

EPS. $0.58 | $0.73 | +25.86%

$838M of buyback.

I believe this reaction is due to very low expectations more than a really strong quarter.

Business.

Bottom line, the core business continues to be very healthy while the excitement continues to build for what's coming next on the app.

Core Business.

Gross Booking Value - the total amount of money spent on Airbnb, is still stable with a 14% YoY growth while FY24 ended with a 12% YoY growth. Airbnb is slightly impacted by currency mix but as most of its business is done in western countries, this impact remains small.

In terms of numbers of bookings, we're with a stable 12% YoY growth. Just a reminder that comparisons have to be done YoY due to holiday seasons, etc…

There is a small inflection in growth for the quarter after three consecutive declining ones, but it's hard to know if this is the start of an acceleration or just a difference in user behavior & timing. We know the team talked about some delays in bookings so this could explain it. For now, I remain with the second option.

On the take rate & daily rate, both remained flatish which is exactly what we want to see as a higher take rate would impact end users’ prices & Airbnb needs to remain competitive. The company has to grow on volume, not take rate - this is detailed in the investment case.

The company continues to expand geographically, with most of its growth coming from new markets - Asia & Latin America. They play their playbook with most investments spent on marketing, with success.

“During the second half of 2024, we introduced brand campaigns more broadly in Latin America, helping to raise awareness and showcase the unique offerings on Airbnb. In Q4 2024, we saw growth in the number of first-time bookers in Latin America accelerate nearly 15 percentage points compared to Q3.“

They also continue to be excellent when it comes to optimizing their application, making it easier for both hosts & travelers to use through plenty of small ameliorations which end up growing retention for both.

And they’ll continue to do so with their new infrastructure, allowing them to leverage AI for translation, customer service & other small but important subjects, constantly improving the app.

This is where Airbnb excels.

Beyong the Core.

This is the big subject around Airbnb, their expansion, the new services they will release during the next months… But nothing yet.

“Today, our service is better than ever, and our platform is ready to support the new offerings we’ll launch as part of our May 2025 Summer Release.“

We’ll have news really soon now & I think this is what built a lot of hope in the stock. Airbnb has always been very good at marketing & is getting much better at attracting & retention; they’ll be very careful on how things are offered & I sincerely hope they will avoid the Booking way, where everything is jumping at you with enormous fees for not much…

“And so, when we think about how to launch these new offerings, we want to be very mindful of the guest journey and to be very thoughtful with regard to both personalization and timing around what type of products are we merchandising to the customer at what point so that we can obviously have the best conversion impact by merchandising the right thing.”

It seems to be the case but we’ll need to wait & see, as we also do not know exactly what will be released.

Besides the new features, some data on the co-hosting system the company released months ago now which I found very interesting, and numbers are very positive.

“In the four months since launching, Co-Host Network has grown to support almost 100,000 listings.”

Incentivizing to maximize the value of their listing is the way to go for Airbnb to grow adoption & retention.

Other.

The company displayed once again how flexible it is, and how valuable its service can become in times of spontaneous higher demand like during the LA fire,

“Airbnb.org, a nonprofit founded by Airbnb, housed more than 19,000 people, including families, first responders, and firefighters—along with over 2,300 pets. Overall, 100,000 free nights have been pledged by Airbnb.org”

This is good publicity for them but again, exactly like during the Paris Olympics or the Euro in Germany, Airbnb shows that their listing flexibility is a really strong asset, capable of freeing tons of space in any city in a few days.

Revenues.

Revenues were also good, stable business equals stable income.

We’re talking about an 11.9% YoY growth for the full year with flat expenses during the same period which means growing margins, jumping from 15.3% to 22.9%. This reflects in the income with pre-tax income growing 58.4% - not including the tax benefit, which isn’t related to the business.

The company closed the year with $8.6B of net debt & $4.48B of FCF FY24, including $1.4B of SBCs which is balanced by the company’s buybacks as the total shares declined YoY.

Airbnb is really healthy & getting better at generating cash. Everything a shareholder wants to see.

Guidance.

The company didn’t give much guidance except to say that they’d expect Q1-25 to be comparable to Q1-24 in terms of growth, meaning high teens, depending on FX impacts.

Conclusion.

I sold my Airbnb position some time ago because I’d rather have liquidity invested elsewhere, in a macro where western travelers start to struggle while the company isn’t involved enough with other region’s end users. You can travel to Japan using Airbnb, but few Japanese travel to Europe using it.

I do not think this quarter proves me wrong. It is a good quarter with a healthy core business & great management. But not much more yet.

There is, however, a lot of optimism about the new features which will be released soon now & I understand the market’s reaction. Airbnb was given away the last months under $130 - as I shared many times here.

In terms of valuation, Airbnb is very hard to judge as we can estimate that the core business will continue on its double-digit growth trajectory. But it is impossible to anticipate how the new features will impact growth - management talks about years before it becomes significant.

At today’s price & only factoring the core business, we’d need lower ratios than the 10Y average but we’d need to factor that Airbnb grew much faster years ago. The company’s 3Y P/S average is at x8, which is a better indicator to me.

My fair value for the company’s core business remains around $130.

I’m still out, still loving the company & still considering it. It’s just hard to find liquidity for it as I prefer all my other holdings over Airbnb at the moment. I might change my mind if the new features convince me & the stock goes back to an attractive price.

Although it is also fair to believe that today's price is the fair price as it includes future growth from those new features. Everyone will have a different opinion on this. Mine remains that anything under $130 was a great entry/accumulation point, but that I preferred to attribute liquidity to other stocks at that time.

No one can buy everything.