Airbnb | Q2-24 Earning & Call

The undercover rocket.

If you need to know a bit more about Airbnb, everything can be found here.

Overview. Another very correct quarter for Airbnb.

EPS. $0.90 | $0.86 | -4.44% miss

Revenue. $2.73B | $2.75B | +0.66% beat

$749M of buybacks - More than $5B left.

"We continue to drive growth by investing in under-penetrated markets. In Q2, growth of gross nights booked on an origin basis in our expansion markets significantly outperformed our core markets on average."

The company is as usual meddling with taxes, impacting net income & EPS but the global business is pretty healthy.

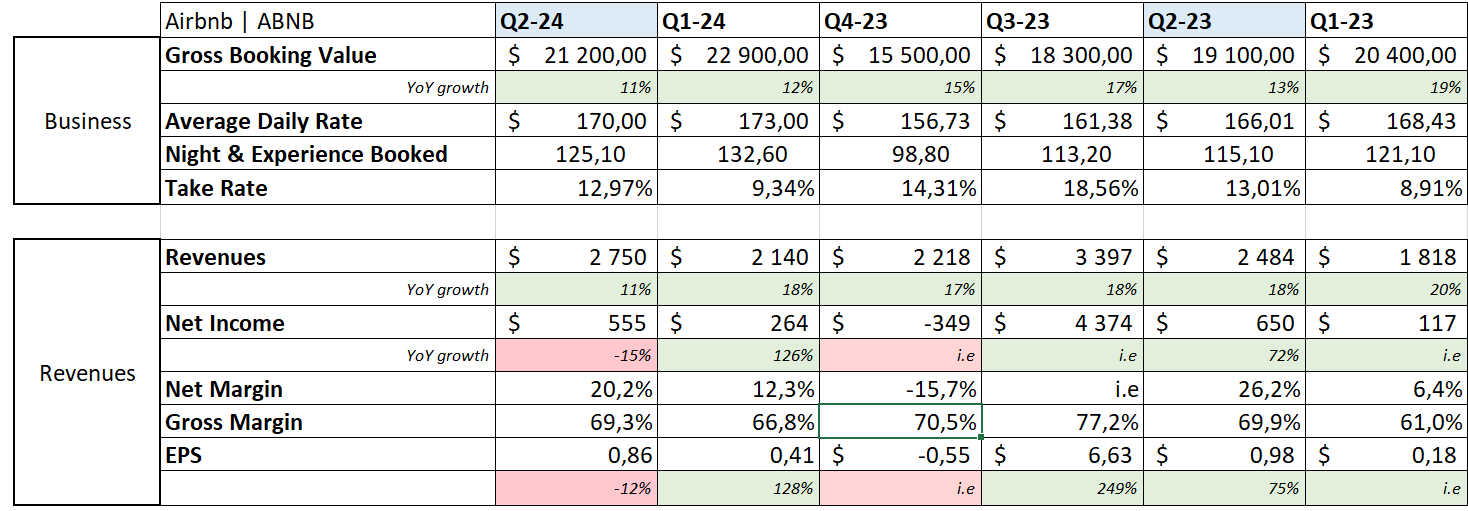

Business.

In terms of pure data, we had a pretty good quarter in terms of growth with +11% of GBV and +9% of nights & experiences booked YoY. While take rate & ADR are staying roughly flat YoY, exactly as they should. Everything is behaving as we want it to.

Management is still focused on offering the best service possible and removed 200,000 listings since April, while the total listings on the platform passed 8M active listings.

The last winter updates saw plenty of interesting features like the “guest favorites,” which also helped raise the overall quality and seemed to have attracted lots of users, as more than 150M nights were booked through this new feature.

In terms of consumers, we’re in the second quarter in a row where first-time bookers are growing rapidly, and bookings through the application are above 55% as the company focuses on driving adoption through the app.

Markets & Consumers. The new markets are logically outperforming the core ones - being the U.S., France, U.K., Canada & Australia. This seems to be a normal tendency, but the truth is growth is also slowing in those core markets.

“However, we are seeing shorter booking lead times globally in some signs of slowing demand from U.S. guests, and our Q3 outlook incorporates these recent trends.“

We’ve talked about it in the last weekly report when the market crashed in fear of a recession. The consumer is getting weaker and we gotta accept it. Airbnb is showing the same tendencies as others: low-income households are struggling while others are still consuming.

"And I think part of the read-through from that can be, oh, people are choosing more expensive listings, therefore, you know, you are seeing stronger demand from higher economic demographics.“

Many users are planning shorter holidays, and there is a tendency not to book holidays too far in advance, something Airbnb already noticed during the COVID pandemic when things were uncertain in terms of regulation back then, and uncertain in terms of budget now.

Again, this was anticipated and is entirely normal - it shouldn’t be attributed to Airbnb’s business. Booking reported its quarter some days ago and showed the exact same tendencies.

Special events. The Euro & Olympic Games bring another proof of Airbnb’s competitive advantage.

“And these events, what they really do is they highlight Airbnb's unique ability to disperse travel and spread economic benefits by allowing people to stay in local neighborhoods where there are no hotels.”

It is valuable for cities to have this kind of solution but also for hosts who can just leave their place for some days while making a few bucks.

“But a lot of people for events coming to town is willing to host one week and make $1,000 or $2,000. And so, what we did is we focused a year ago on Paris. And in the last year, we increased our supply in Paris by 37%. We now have nearly 150,000 homes in Paris.”

No other platform can do anything like this, as hotels cannot create new rooms when demand rises for example. This is on of Airbnb’s strength and we will see it more & more in the future.

Beyond the core. We do not have much more information on what’s coming, but Brian confirmed we will have more details next year and hinted again to some ideas.

“We're going to have to do multiple new things. We're going to have to have multiple new products and multiple new services [...] It's going to be about long-term stays. It's going to be our guest services, host services, and many new offerings. And you'll begin to see that next year.“

But we had a few more concrete plans like a co-hosting marketplace & a complete review of the system of experiences. For the first one, here’s Brian’s vision:

“So, there are people that have homes, but they don't have time. There are other people in the world that have time, but they don't have a home. And so, there's a Venn diagram of people today who have both and can host. But what if we can match those two people together? That would unlock a lot more inventory.”

Reworking the experience is also very important in my opinion, as they said themselves.

“I mean, a lot of people, they come to our homepage, they don't ever see experiences.”

And they intend to propose those experiences differently.

“So, we're going to completely reimagine our search and discovery engine to cross-sell experiences after you book a home.“

This is a very good idea and will certainly boost the take rate because many vacationers end up doing activities, but none of them really look on the Airbnb app - I certainly don’t. But more will come as this isn’t exactly beyond the core.

“And I do think Airbnb will eventually be much more than a search box where you type a destination, add dates, and find a listing. it's going to be much more of a travel concierge. It's having a conversation, learning, adapting to you.”

Brian also detailed during the call that reaching this kind of product will take time, years, as leveraging AI at the software level wasn’t as easy as many would think - it requires to re-build apps almost from scratch as the infrastructures are not the same at all. But he confirmed that they are already working on it, but again, it will take two to three years to get there.

Airbnb has the community, the data, and many exclusivities. It will become the travel concierge we want it to be but we gotta be patient.

Revenues.

Things could of course be better here but everything is correct.

Few important points to note though.

Growth has slowed this quarter, dropping below 15% for the first time and this is tough on the statement because it highlights the increase in expenses. There's a lower operating income for the quarter and a decline in net income YoY - due to a higher tax rate.

I also highlighted the YoY comparison for the six months ending to show that this difference is only for the quarter. H1-24 is stronger - revenues are up +13.6% while net income is up +6.8%.

Yet, as we’ll see with the guidance, growth will continue to slow down and management plans to increase expenses, especially in marketing, during the second half of the year - which means margins will continue to shrink. This should be seen as an investment to grow faster in under-penetrated markets and will certainly pay off in network effects later on.

In terms of balance sheet, the company is closing this quarter with $8.3B of net debt, $1B of FCF for the quarter & $4.3B TTM. Very, very comfortable position.

I’ll quickly talk about buybacks. The company still has $5.25B left on its current plan, which represents more than 7% of the company at today’s valuation - after the stock was oversold because the market considered the business a failure while the issue is with the macro.

I’ll just share here my vision on Airbnb in one image.

This doesn’t even talk about the business itself and how it doesn’t have any competition. It doesn’t address the potential to expand into other services while they have the brand, the user base & the data. It doesn’t mention how great management is or that the company is still founder-led.

This is only about how much money the company has and is making. We’re talking about more than 40% net income and FCF margin with $8.3B in net debt. More than a third of their revenues is available to be either reinvested into R&D or returned to shareholders.

Yes, growth is slowing, but this has nothing to do with the business and it will re accelerate in a better environment. We’ll talk valuation a bit further.

Guidance.

This is what is hurting the stock today, as once again, the threat of recession is upon us, and it’s starting to show in some companies.

As mentioned above, slower growth due to lower demand due to a tough macro, coupled with bigger expenses equal lower margins. But again, this isn’t specific to Airbnb, Booking had exactly the same kind of weak guidance.

“What I would say additionally is that, you know, over the last couple of years, as we emerged from COVID, there were several periods where we saw, you know, some volatility in terms of overall lead times and, in particular, some hesitancy for consumers to book those longer lead time trips. I suspect that's what we're seeing right now.”

This is what the market interpreted as “Airbnb is over.” I think very differently.

My Take.

You will need to read the investment case linked at the top to understand how strong Airbnb's business is and to review other companies to understand that its slower growth isn’t due to internal issues, but to larger economic conditions. The company will likely struggle over the next few months, maybe a year or two, but what will emerge will certainly be worth investing in now - only my opinion.

Either way, struggles are to be expected.

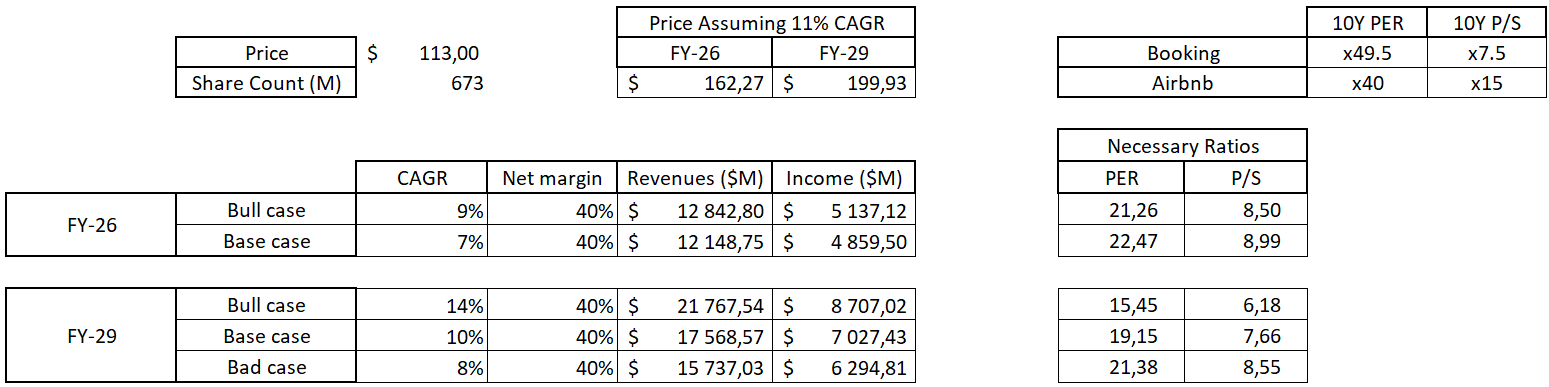

In terms of valuation, I already considered Airbnb fairly priced around $140 and this quarter doesn’t change my opinion at all. I knew it wouldn’t shine - and it kinda did good compared to a Q2-23 with Easter included, but what matters are the next few years.

The stock closed the day at $113 and should continue to grow in the middle to high single digits over the next two years, even accounting for a recession - already up +13% H1-24 YoY. Assuming margins stay flatish YoY, which they should or at least are guided to, Airbnb would need to trade under 23x PER and 9x P/S to reach our 11% CAGR on investment. The ratios necessary for 2029 are of course much lower, while the growth expectations should be higher.

We’re talking about a company planning to expand its current business geographically and develop new services and products over the next few years - something that will certainly reaccelerate growth, and they have the margins and cash to do so without any struggle.

It’s hard for me to understand the pessimism around this stock, and as you’ve understood, I’m a buyer here. Slowly, because I expect the stock to struggle for a while, but I plan to build hell of a position over the next few months.

Remember, this isn’t advice, just my opinion.