Adobe Q2-25 | Earning & Call

Is the famous disruption in the room with us?

Everything you need to understand Adobe is here.

Adobe | Investment Thesis

Pretty sure you guys already know Adobe, if only for its PDF reading software or its famous Photoshop. Both come from the same house, but there’s much more to say about the company.

“The creative opportunity is expanding across audiences with AI as an accelerant. It is opening the content floodgates, tapping into everyone's imagination, and massively expanding the number of creative assets being created, edited, integrated, and delivered.”

Overview.

Revenue. $5.8B | $5.87B | +1.26% beat

EPS. $4.97 | $5.06 | +1.81% beat

$3.5B buyback.

Business.

The market continues to talk about the upcoming disruption of content creation, but Adobe’s numbers continue to prove that nothing of the sort is happening, or at least that they have what it takes to keep their leader position in the sector.

As I detailed in the Investment Thesis, what makes Adobe different is not its individual softwares, it is their ecosystem which has no competition.

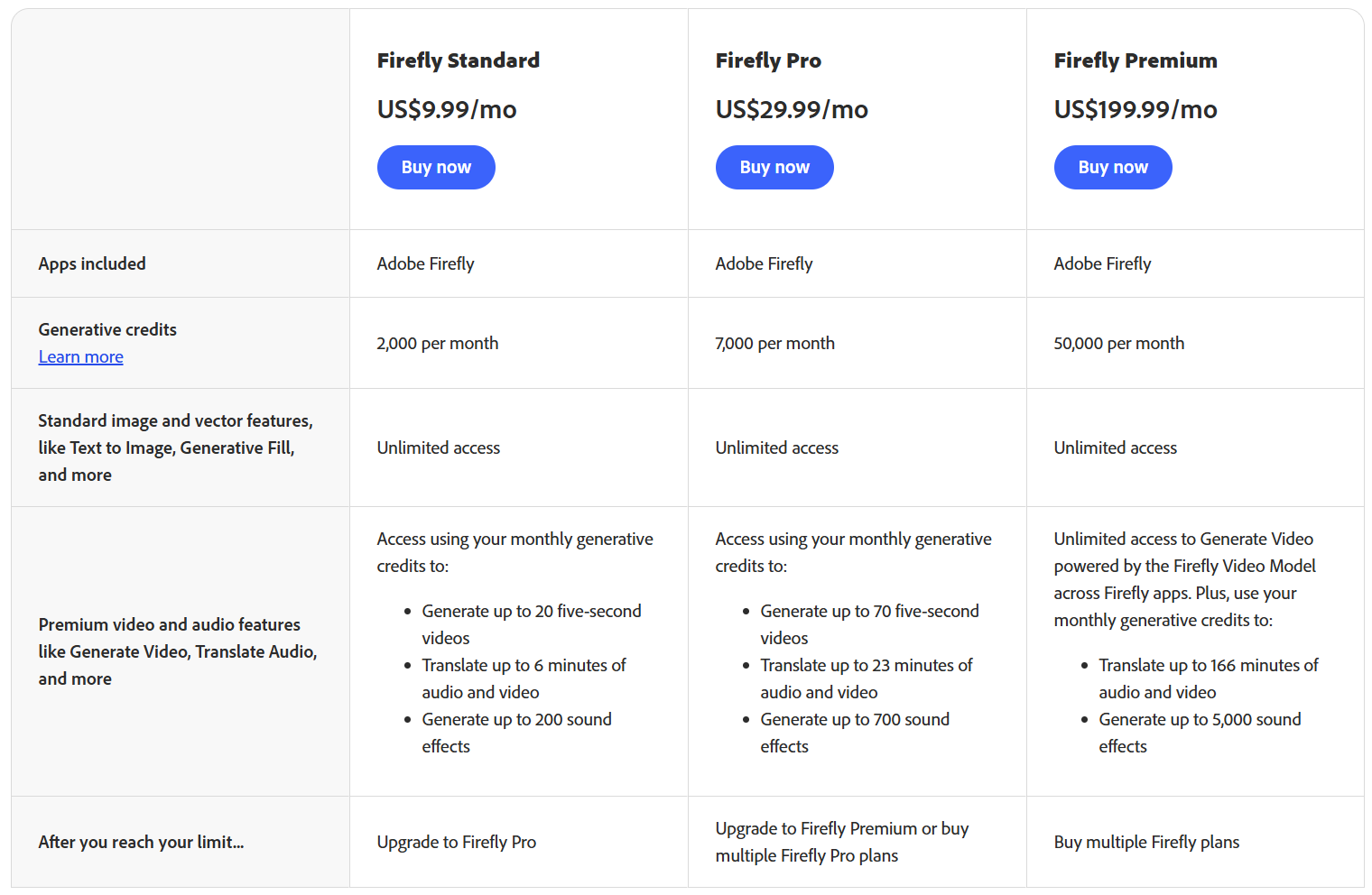

“Firefly empowers creative professionals to generate images, video, audio, and vectors from a single place with unmatched creative control, iterate on their creations through Adobe's creative apps, and seamlessly deliver them into production.”

While any LLM will allow you to create any kind of content, Adobe’s Firefly will not only do the same - with better quality most of the time, but it will also allow you to retouch your content - video & image, test different marketing campaigns through different platforms & collect data from each to find the most engaging version.

ChatGPT, Llama, MidJourney & co cannot propose anything comparable; they will generate images but professionals would then not have the opportunity to modify them, to build marketing campaigns nor to extract data from those. This is Adobe’s value proposition: a complete advertising ecosystem.

“Firefly empowers creative professionals to generate images, video, audio, and vectors from a single place with unmatched creative control, iterate on their creations through Adobe's creative apps, and seamlessly deliver them into production.”

Even better, Firefly is composed of its own AI generative model but also proposes to access ChatGPT’s, Meta’s Llama, Google’s Gemini & more. Any subscriber could access and try competitive tools from Firefly and still access the entire Adobe’s ecosystem.

And this is what is attracting users, households & companies.

“Traffic to the Firefly app grew over 30% quarter over quarter and paid subscriptions nearly doubled in the same period. Firefly continues to drive new user acquisition with first time Adobe subscribers growing more than 30% quarter over quarter.”

For now, Firefly is a standalone subscription but Adobe plans to include it in bundles.

This is Adobe’s value proposition and there are no competitors to it, as it goes much further than simply generating some images from our bedrooms.

And demand is still really strong with a 15% YoY subscription growth from business with Adobe Express being a huge source of growth - their cloud-based solution to leverage Firefly more simply than through their softwares.

“The Express ecosystem continues to expand with partner add ons growing more than 25% quarter over quarter with new integrations from Google Ads, Vimeo, and Bitly. Select key global customer wins include Cisco, County of Los Angeles, the Defense Information Systems Agency, Macy's, and Ulta Beauty.”

Adobe has to be observed as a complete service leveraging AI by now. Not as three branches with different business & revenue stream.

Financials.

It is easy to generate cash when all your branches are growing double-digit YoY with strong sequential momentum.

Six months revenues are up 10.4% YoY with gross margins expanding from 88.6% to 89.1% which isn’t a huge expansion but is notable as the company expands its AI portfolio. Income comparison is positively impacted by the $1B termination fee last year but we still have really strong numbers with $3.5B of net income for a 30% net margin. Really. Strong.

In terms of cash, Adobe has a flatish net debt for $2.2B operating income and reduced shares outstanding -4.8% YoY as the stock price is depreciated, giving opportunities to return value to shareholders with $10.9B left on their program.

Guidance.

Adobe raised its FY25 total revenue & Digital Media guidance following the strong demand of this quarter, which again doesn’t highlight any potential disruption.

“If you do the math, our core creative business, subscription revenue has been accelerating over the past few quarters.”

Revenues to be expected between $23.5B & $23.6B or up 9.5%.

Valuation.

This model assumes a 10% & 7% CAGR growth until FY26 & FY29 respectively, 30% net margins, 3% of return to shareholders & P/S & P/E at 10x & 40x respectively, Adobe’s 3Y average.

Fundamentals assumptions are close to market & management’s expectations but as often, the ultimate question is about deserved multiples. The software sector always had high ones and I believe Adobe continues to deserve them but the market is worried about this famous potential fundamental disruption.

Being more conservative with multiples at 8x & 35x for P/S & P/E respectively would bring Adobe’s fair price around $380.

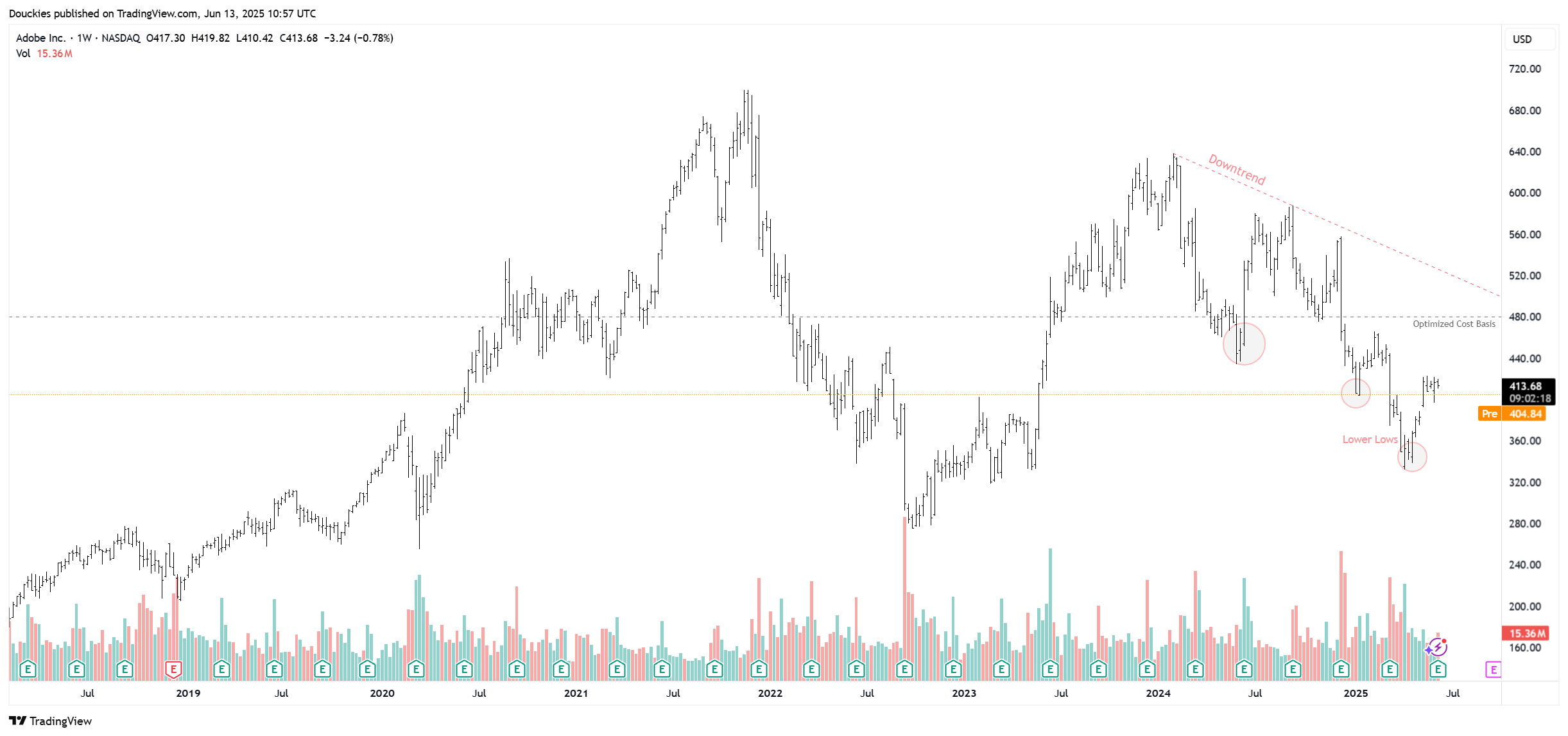

In my case, price action will be the determinant factor of when I will buy in, assuming that fundamentals do not change until then. For now, the stock continues on its downtrend without any consolidation in sight.

This is why I do not buy downtrends. Anything can happen even if we already trade much lower than what I assume to be an optimized accumulation price. Patience is important in the markets to maximize returns.

My Take.

Management says it better than I.

“Adobe is the only company unifying the entire workflow from creation and production, workflow and planning, asset management, delivery and activation, through to reporting and insights.”

And this is what data is reflecting, whatever our personal bias.

What do you think multi-billion-dollar companies will choose between ChatGPT text-based generation tools & a complete ecosystem allowing leveraging AI to generate & optimize content, manage different marketing campaigns and collect precise data for each of them from different social media points to then be able to tweak your content in order to generate maximum engagement?

LLMs are great, but they won’t disrupt everything by themselves. AI will, and winners will be companies capable of leveraging it.

Adobe is one of them and data proves this.