Adobe | Q2-24 Earning & Call

The market only needed one thing for Adobe: A confirmation that their products are still in demand and that the new trendy tools wouldn’t replace them. It seemed like an obvious fact for some, but the market didn’t see it that way.

Overview. One thing for sure: Adobe delivered, beating its own quarterly revenues & EPS guidance, which doesn’t happen often.

EPS. $4.39 | $4.48 | +2.05% beat

Revenue. $5.29B | $5.31B | +0.36% beat

4.6M shares bought back for $2.5B | $22.7B remain.

"Our market-leading products, strong execution and world-class financial discipline position us well for the second half of 2024 and beyond."

As advertised: This isn’t the profile of a company whose products aren’t demanded anymore.

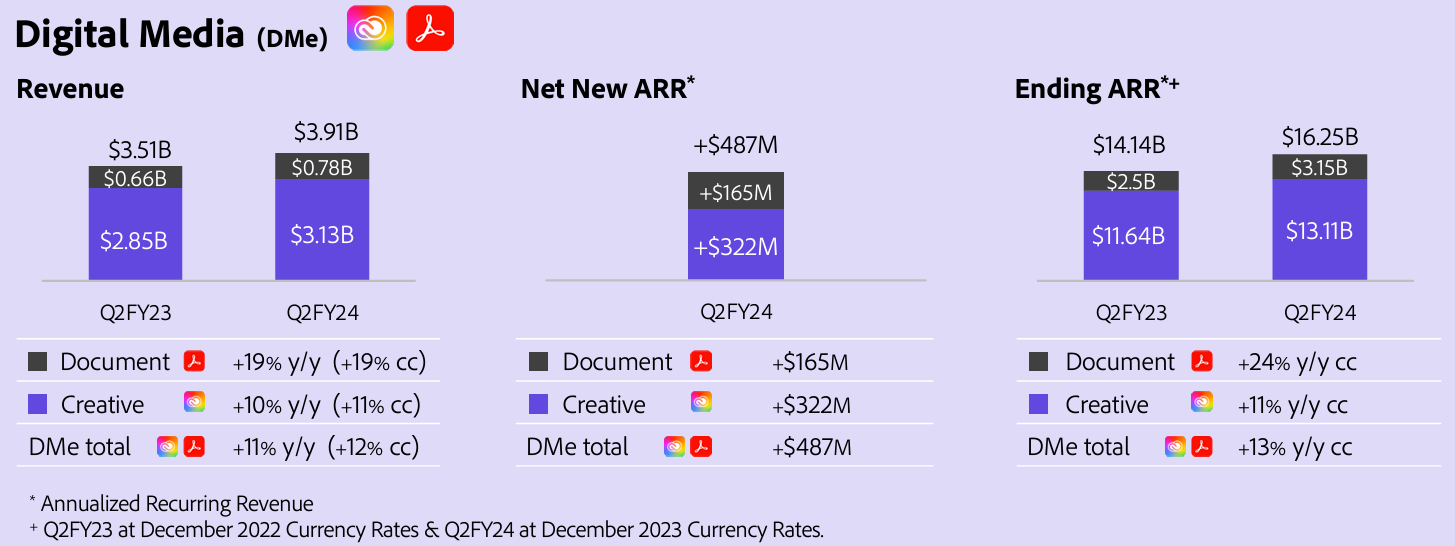

Business. Digital Media is still the biggest source of revenue, growing strongly thanks to new customers, growing usage of their apps & subribers upgrading their subscription plans thanks to the new Firefly tools.

As a reminder, this branch includes Adobe’s creative softwares. A growth above 10% indicates a strong demand for those tools and that creators did not find alternatives, not with ChatGPT, MidJourney, Sora or any other text-based soft. Why? Because management understood AI is only a tool, not a replacement for human creativity.

“Adobe’s highly differentiated approach to AI is rooted in the belief that creativity is a uniquely human trait – and that AI has the power to assist and amplify human ingenuity and enhance productivity.“

But they are not staying behind nor away of AI; they are creating their own tools with the Firefly suite. These are just different from text-based prompts and will answer their users’ needs, not try to replace their work.

“Generative Fill and Generative Expand are already two of the top three features used by customers on the latest version of Photoshop. Text to vector support is off to a great start in Illustrator. Remove Object is the fastest growing feature in Lightroom mobile. Our preview of generative AI capabilities in Premiere won Production Hub Award of Excellence at NAB, the largest video show in North America. We are integrating our leading applications with Firefly and third-party generative AI models to deliver the richest, most engaging content.“

And for those who like to use text-based generative tools, Adobe also proposes one with its Firefly suite. Anyone who has a subscription to one of their products will be more likely to use the in-house text-based prompt than to pay for a ChatGPT or MidJourney subscription.

“These integrations are driving the acceleration of Firefly generations, with May seeing the most generations of any month to date.“

My global opinion didn’t change: If you ever used one of Adobe’s software, you know text-based AI won’t replace it; if anything, it will amplify demand as users will be able to generate more content that will need modifications through Photoshop, Premiere, or any FX soft.

It’s a positive catalyst, not a risk.

I do not think there were lots of concerns around the Digital Experience branch nor the Cloud one, which are both growing properly - as expected. With a very special mention to the Document Cloud branch, growing faster than ever thanks to some new AI summary tools developed over the last months which improved users’ experience.

“Acrobat AI Assistant is empowering everyone to shift from reading documents to having conversations with them – in order to summarize documents, extract insights, compose presentations and share learnings.”

but what really matters is that the Digital Media branch is growing strongly and that demand isn’t slowing.

Results showed that growth is good, the net ARR show that demand is still there for the next months at least - and longer in my opinion & RPO is up to $17.86B, +17% YoY.

Only positives.

Revenues. Unsurprisingly, data is good here as well.

Both net & gross margins improved due to both revenue growth & better execution with kind of flat cost of revenue & slowly growing operating expenses - only up +7.8% YoY. All those factors result in a record net income for the company.

The balance sheet remains strong with more than $2B of net debt & OpCF is impacted by changes in deferred revenue but is still strong at $1.94B.

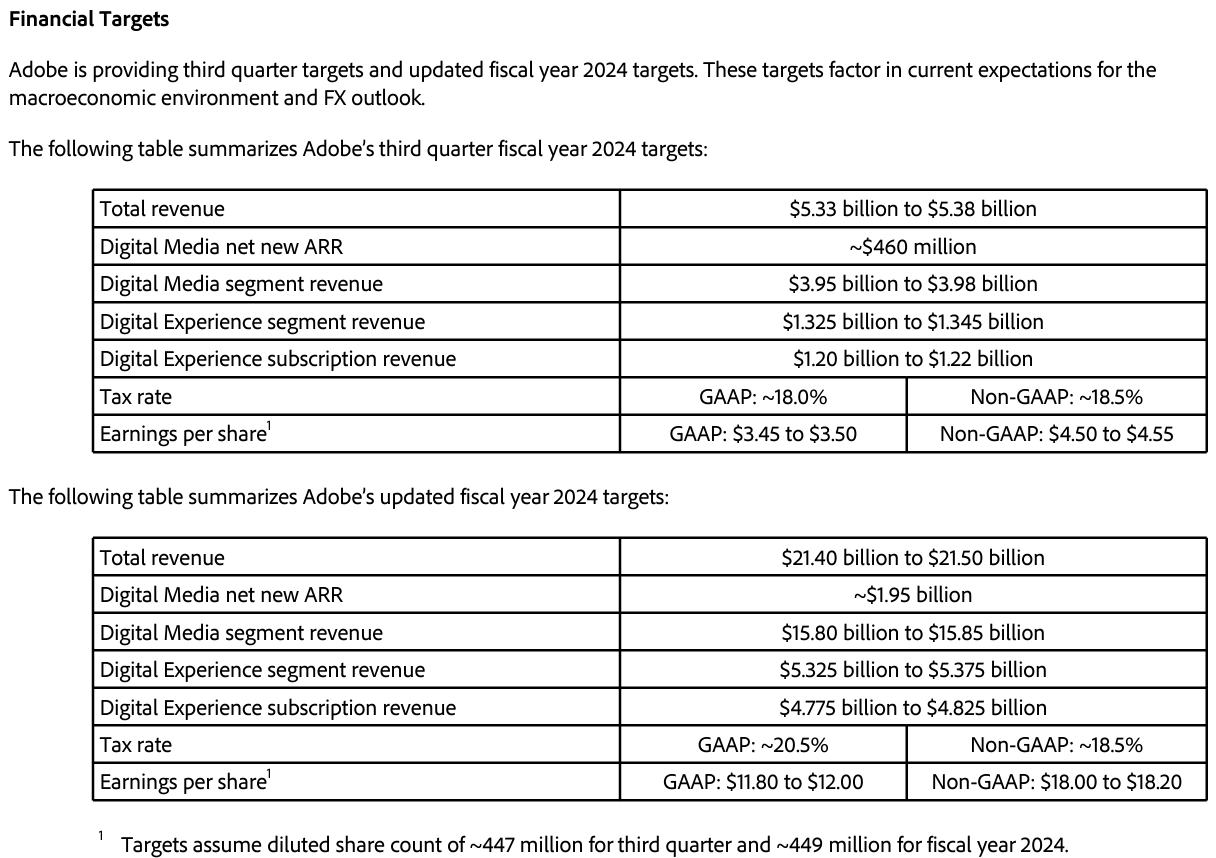

Guidance. Another very strong point of this report is Adobe raising its FY-24 guidance - again, proof of strong demand.

Conclusion. Adobe clearly understands its business & challenges and is responding to them perfectly. AI can disrupt their business? Then let’s take any tools which could do so and integrate them into our products. They even made them better as their in-house tools are much more personalized to their users' needs.

It will take more to disrupt Adobe and its products. Much more. And the market might be starting to realise it.

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!