Abode | Q3-24 Earning & Call

First signs of weakness or just a bump?

If you do not know Adobe, they are the parent company to many software that everyone knows: Reader, Photoshop, Premiere, Illustrator & many more. A very important company which many are calling doomed because of AI text-based generative images.

I think the contrary.

Overview.

We're on a pretty good, even strong quarter.

EPS. $4.53 | $4.65 | +2.65%

Revenues. $5.37B (est) | $5.41B | +0.71% beat

$2.5B of buybacks.

“Adobe had an outstanding third quarter. We saw strength across Creative Cloud, Document Cloud and Experience Cloud. Our success reflects our strong execution against an ambitious innovation agenda to deliver value to Page 3 of 22 our customers.”

The overview says it all, a very constant company.

Business.

I'll start again with a laius on why - to my opinion, AI & text-based content generation tools (like ChatGPT & Sora) are a catalyst for Adobe and not threats, at least for their Creative Cloud business portion - the biggest source of revenues. I have two arguments for this.

Catalysts. Text-based generation tools are just this: tools. They are not serious software for now, and even if they become some, it will only generate more demand for Adobe's software, not less. No creative will be able to generate exactly what they want from text-based tools & they will need other software to shape this raw content to their will. And only Adobe proposes performant enough software to do so.

In-house. Secondly, many forget that Adobe isn't behind at all when it comes to AI tools; they propose software as performant - if not more, with Firefly. We saw that during the last Adobe MAX presentation, and things have gotten better since - and will probably be even better in their next presentation next month. If anything, they have a huge advantage over competition by being able to use Firefly, one single software, through all of their applications, proposing more for less.

“Our greatest differentiation comes at the interface layer with our ability to rapidly integrate AI across our industry-leading product portfolio, making it easy for customers of all sizes to adopt and realize value from AI.”

It goes further.

“Firefly-powered features in Adobe Photoshop, Illustrator, Lightroom and Premiere Pro help creators expand upon their natural creativity and accelerate productivity. Adobe Express is a quick and easy create-anything application, unlocking creative expression for millions of users. Acrobat AI Assistant helps extract greater value from PDF documents. Adobe Experience Platform AI Assistant empowers brands to automate workflows and generate new audiences and journeys. Adobe GenStudio brings together content and data, integrating high-velocity creative expression with the enterprise activation needed to deliver personalization at scale. Overall, we’re delighted to see customer excitement and adoption for our AI solutions continue to grow and we have now surpassed 12 billion Firefly-powered generations across Adobe tools.“

As usual, Adobe's advantage is in its Creative Cloud, allowing its users to have access to the best-in-class content creation softwares, all linked together. And demand for those new products is real, from every demographic & sector as content is becoming more & more important in our world - for advertising, presentations, communications, etc...

“We’re thrilled to see this value translate into AI Assistant usage, with over 70 percent quarter over quarter growth in AI interactions.“

I just want to point out that text-based generation isn't the only functionality Adobe is proposing; they are also improving their software with much more than "just" image generation.

Who would want to use ChatGPT or Sora when you have a product like this? This is for the actual state of Adobe, AI, & how the company is improving its software.

They're not behind.

Adobe Reader. A small word on Document Clouds as revenues from this section grew 18% YoY with a rapid & strong increase of MAUs in-app & through third parties. Most of the revenue growth comes from the new AI functionalities which are becoming very, very useful when parsing a PDF.

This isn't the biggest revenue for the global company, but it is good to see this part growing that much - a tendency which should continue.

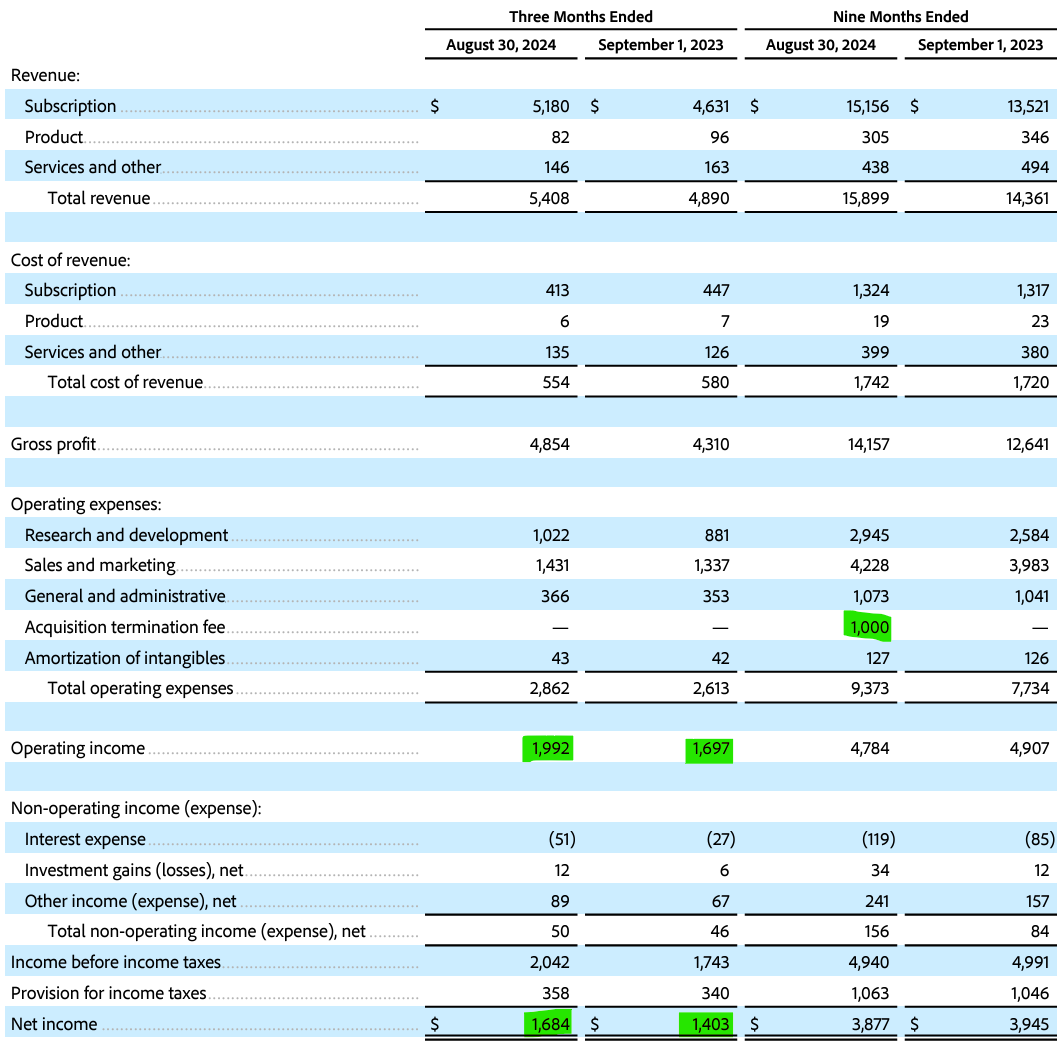

Revenues.

The quarter was pretty strong.

Besides a very stable growth, we can see a real improvement in terms of execution with operating & net income's margins growing - except in the 9 months ending because of a one-time expense.

Adobe closes the quarter with a $3B net debt & a $1.9B FCF.

Guidance.

This is what the market did not like and which could actually go against everything I wrote above. Why would Adobe expect slower growth if its products are still demanded & AI is growing monetization?

We'd be talking about 10% YoY for Digital Media & only 7% for Digital Experience for a global growth under 10% for the first time since... years. It's hard to give a reason as I didn't find any answers on the earnings call.

This is but one quarter's guidance, so we'll need to wait to figure things out.

My Take.

The conclusion is pretty easy for this quarter: Strong revenues & execution with a steady business, improving products & offerings. Yet, the guidance doesn't reflect the quarter's strength nor my optimism on the business's strength & advantage over competition.

This isn't a big issue for me as I am not a shareholder and am patiently waiting to buy in, so I can wait a few more months to have confirmations, especially as we're not where I want yet in terms of valuation.

I would not think about buying Adobe above its P/S medium even with a decreasing P/E ratio as this comes with buybacks & better execution. It is important, but I think focusing on P/S makes more sense for this case, and buying above x11 seems expensive, especially with lower guidance.

This quarter doesn't change anything to my position: Waiting for a proper entry price while monitoring the company. If the slower growth is indeed due to a lack of usage of their applications, i’ll revisit my thesis.

But we’re not there yet.